TL;DR:

- Choosing a jewelry payment plan requires understanding options like layaway, BNPL, and in-house financing, each with different risks and benefits. Careful preparation, including proof of income, ID, and budget planning, helps manage the risks of interest charges, late payments, and deferred interest traps. Balancing ethical sourcing, personalized design, and financial comfort ensures a meaningful, stress-free engagement ring purchase that aligns with your values and budget.

Choosing the perfect engagement ring or wedding band is one of the most exciting moments of your life, but it also comes with a real financial weight. The piece you both love might cost more than you can pay upfront, and that tension between dream and budget is something almost every couple feels. Payment plans can close that gap, but only when you use them wisely. This guide walks you through exactly how to prepare, apply, and manage a jewelry payment plan so your milestone moment comes with joy, not debt regret.

Table of Contents

- What to know before using a jewelry payment plan

- Step-by-step: The jewelry payment plan process

- Common mistakes to avoid in payment plan jewelry

- Choosing ethical, personalized jewelry while financing

- The comfortable truth about jewelry financing most buyers miss

- Dream ring, smart plan: How Bel Viaggio Designs helps

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Budget for a down payment | Most jewelry payment plans require a 20-50% initial payment to get started. |

| Choose safe financing | Opt for BNPL or layaway to minimize credit risk and avoid high post-promo interest rates. |

| Avoid deferred interest | Read the fine print to steer clear of hidden fees and costly deferred interest traps. |

| Prioritize ethical, custom choices | You don’t have to sacrifice values or style when you use smart, ethical jewelry financing. |

| Finish without regret | A successful financing plan means ending up with your dream jewelry and financial peace of mind. |

What to know before using a jewelry payment plan

Before you sign anything or hand over a deposit, it pays to understand what you’re actually agreeing to. Jewelry payment plans come in several different forms, and each one carries its own set of rules, risks, and benefits.

The three most common options are layaway, Buy Now Pay Later (BNPL), and in-house financing. Layaway means you pay the jeweler in installments and only receive your ring once it’s fully paid. BNPL lets you take the jewelry home immediately while spreading the cost over weeks or months. In-house financing is closer to a traditional loan, sometimes with promotional interest rates that can flip into high-rate debt if you miss the payoff window.

| Plan type | Take jewelry home first? | Credit check? | Interest risk |

|---|---|---|---|

| Layaway | No | Usually none | Very low |

| BNPL | Yes | Soft check (usually) | Low to moderate |

| In-house financing | Yes | Hard pull (often) | Moderate to high |

When it comes to protecting your credit score, BNPL with a soft credit check is safest for most buyers, since it doesn’t leave a hard inquiry on your report. Deferred-interest plans, on the other hand, are a different story. These plans look attractive because they advertise “0% interest,” but if you haven’t paid the full balance by the end of the promotional period, you get charged all the accumulated interest retroactively. That surprise bill can be hundreds of dollars you weren’t expecting.

Here’s what you should prepare before applying:

- Proof of income. Pay stubs, bank statements, or tax returns depending on the jeweler’s requirements.

- Valid government-issued ID. Standard for any financing application.

- Your target budget and down payment. Plan to have between 20% and 50% of the total cost ready upfront, which is the typical range jewelers expect.

- A list of questions about fees. Ask specifically about late payment penalties, early payoff benefits, and what happens if you need to cancel.

- Your credit score. Pull it yourself (a soft check) before applying so you know where you stand.

Pro Tip: Before committing to any jeweler’s financing, check out options for affordable ethical jewelry shopping to see whether a sale piece can reduce how much you need to finance in the first place. Sometimes the smartest move is starting with a lower base price.

If you’re also researching where to buy, reading up on ethical engagement ring shopping will help you pair smart financing with values-driven sourcing, which matters more than most buyers realize until after the purchase.

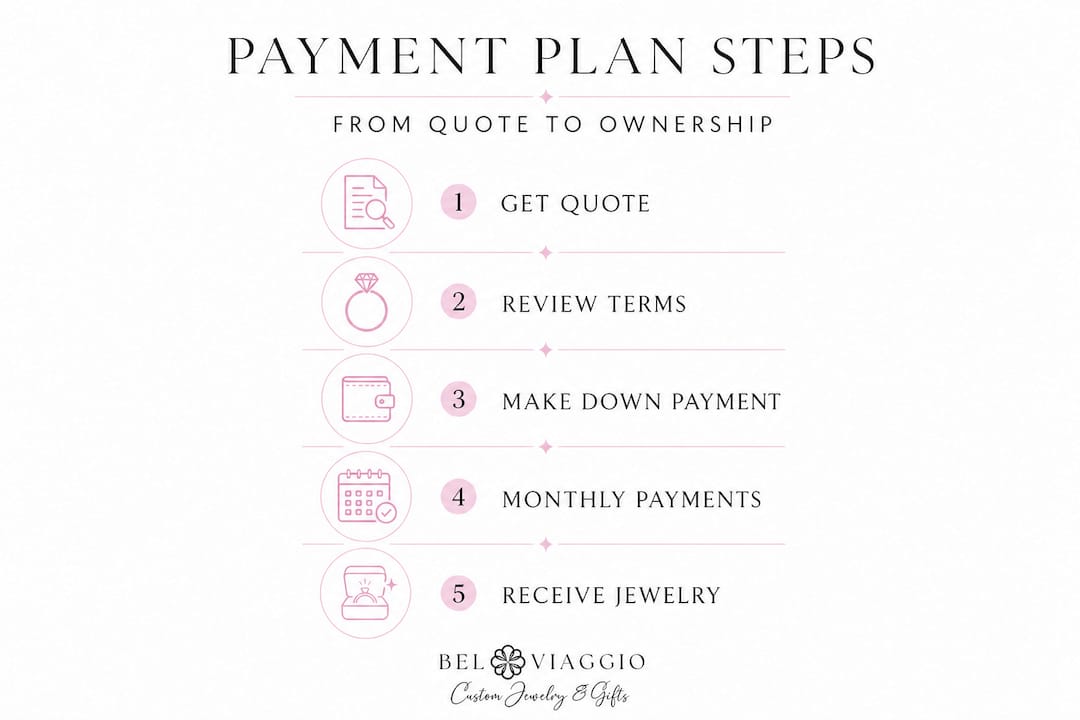

Step-by-step: The jewelry payment plan process

Preparation sets you up for success, so let’s walk through exactly how to execute the process with confidence.

-

Choose your jewelry and request a detailed price quote. Get the full cost in writing, including any customization, engraving, or stone upgrades. Vague quotes create budget surprises later.

-

Ask the jeweler what payment plan options are available. Not all retailers advertise every option upfront. Ask specifically about layaway, BNPL, and any in-house financing programs. Find out the minimum and maximum financing amounts.

-

Submit your application with required documents. This typically means providing proof of income and a valid ID. Some BNPL apps let you apply in under two minutes through a smartphone.

-

Review the plan terms carefully before signing. Note the APR (annual percentage rate), any origination fees, the payment timeline, and the down payment amount. If the APR is above 20%, consider whether a different plan or a smaller ring budget makes more sense.

-

Make your down payment and lock in your order. For custom rings, this often triggers the design and production process. Explore the custom ring deposit process to understand what that first payment covers and what protections you have.

-

Set up automatic payments or calendar reminders. Missing even one payment can trigger penalties or, in a layaway plan, forfeit your deposit. Automation removes the human error.

-

Watch for early payoff benefits. Some plans reward you for paying ahead of schedule by waiving remaining interest. If you come into extra cash, put it toward the balance.

-

Receive your jewelry and confirm everything matches your order. Inspect the stone, the setting, and any custom details before you leave the store or sign for a delivery.

| Payment stage | Key action | Risk if skipped |

|---|---|---|

| Quote stage | Get full cost in writing | Hidden fees surprise you |

| Application | Compare multiple BNPL options | Miss a better rate |

| Signing | Read APR and promo period | Deferred interest shock |

| Active repayment | Set auto-payments | Late fees, credit damage |

| Payoff | Confirm balance cleared | Lingering interest charges |

Financing boosts immediate joy but introduces debt risk, while layaway and BNPL are generally safer choices for buyers who are still building their credit history. Choosing the right structure for your financial situation matters far more than chasing the lowest advertised rate.

Pro Tip: Many jewelers who offer flexible plans, including options to buy now, pay over time, will work with you on a custom payment schedule if you ask. The advertised plan isn’t always the only option on the table.

Common mistakes to avoid in payment plan jewelry

Following the steps is critical, but knowing where others stumble is just as important.

The most damaging mistake buyers make is missing payment deadlines. Even one late payment on a BNPL plan can mean steep late fees. On a layaway plan, missing multiple payments can cause you to forfeit a portion or all of your deposit, depending on the retailer’s policy. The ring stays in the case, and your money stays in the jeweler’s pocket.

Deferred interest is the second biggest trap. That 0% promotional period sounds like free money, but high jeweler APR post-promo kicks in hard after the promotional window closes. If you owe $500 on a $2,000 ring when the promo ends, you could owe interest on the full $2,000 from day one of the purchase, not just the remaining balance. That’s a structure designed to punish procrastinators.

“Always ask whether the plan is ‘no interest if paid in full’ or ‘deferred interest.’ They sound the same, but they are very different in what they cost you.”

Other costly errors to watch for:

- Stretching into a term that’s too long. A 36-month plan on a $3,000 ring might have comfortable monthly payments, but you’ll be paying for the ring well past your first anniversary. That can feel emotionally heavy.

- Ignoring the insurance and return policy fine print. Some financing plans void the jeweler’s return window once you activate a payment plan. Others require you to purchase insurance separately. Know this before you sign.

- Buying above your real budget by banking on a future raise. A promotion or new job isn’t guaranteed. Budget based on your current income, not your projected one.

- Not getting everything in writing. Verbal promises about upgrade policies, trade-ins, or fee waivers mean nothing without documentation.

Pro Tip: Before you fall in love with a specific price point, read up on why investing in fine jewelry makes financial sense when done right. Understanding the long-term value of ethically sourced pieces helps you see the bigger picture beyond the monthly payment.

Choosing ethical, personalized jewelry while financing

Avoiding mistakes is easier when you know what you want, so let’s discuss how to balance the desire for custom, ethical jewelry with financial wisdom.

One of the most common fears couples have when financing is that they’ll have to compromise on quality or values to stay within budget. That’s not true. Ethical, personalized jewelry is absolutely achievable with a payment plan, as long as you plan strategically.

Here’s how to keep your values and your budget aligned:

- Prioritize stone sourcing transparency. Work only with jewelers who can verify where their diamonds, moissanite, or gemstones come from. Lab-grown diamonds, for example, offer the same brilliance as mined stones at a significantly lower price, which reduces how much you need to finance.

- Choose customizations strategically. Not every design detail adds equal emotional value. Decide which elements matter most to you, whether that’s a unique band shape, a specific engraving, or a particular stone cut, and allocate your budget there first.

- Ask about flexibility in the financing for custom orders. Some jewelers allow you to start a payment plan before the ring is finished, spreading the cost across the production timeline.

- Use your down payment to reduce the financed amount. Budgeting 20-50% down upfront lowers your monthly obligation and reduces the total interest paid over the plan’s life.

- Don’t confuse price with value. A custom ring built with ethical materials and real craftsmanship often holds its value better than a mass-produced piece at the same price point.

Exploring custom jewelry benefits before you start the financing process can shift your entire mindset. When you understand what makes a piece truly one-of-a-kind, it’s easier to spend intentionally rather than impulsively. And for specific inspiration, ethical custom ring ideas can help you visualize what’s achievable at different price points.

The comfortable truth about jewelry financing most buyers miss

With the process mapped out, it’s worth taking a step back and reflecting on what really matters when financing jewelry.

Most buyers fixate on the monthly payment number. They calculate what they can squeeze out of a paycheck and work backward to a ring budget. That approach isn’t wrong, but it misses something important: how it will feel to still be making payments six months after your engagement, or twelve months after your wedding.

There’s a real emotional cost to carrying debt through milestone moments. Your engagement should feel like freedom and celebration, not a monthly reminder that you overstretched. The couples who look back on their ring purchase with zero regret are rarely the ones who found the lowest APR. They’re the ones who found a plan that ended before it became a burden.

That’s why we believe the best payment plan isn’t the cheapest one on paper. It’s the one that aligns with your values, your timeline, and your emotional bandwidth. A shorter plan with a slightly higher monthly payment often means finishing with pride instead of fatigue. A jeweler who shares your ethics means the ring carries meaning beyond its sparkle.

Value-driven engagement ring shopping is about recognizing that the smartest financial decision and the most meaningful personal decision often overlap. Sometimes that means choosing a lab-grown stone. Sometimes it means a shorter financing term. Almost always, it means being honest with yourself about what you can genuinely afford without stress.

The goal isn’t just a beautiful ring. It’s a beautiful ring and financial peace of mind on the other side.

Dream ring, smart plan: How Bel Viaggio Designs helps

Ready to shop with both confidence and conscience? Here’s how Bel Viaggio Designs can help make your dream ring a reality.

At Bel Viaggio Designs, every piece is handcrafted with verified ethical sourcing, from lab-grown diamonds to stunning moissanite and gemstone options. You’re not choosing between beauty and responsibility. You get both.

Flexible payment options, including layaway and buy now, pay later plans, are designed to fit a range of budgets without forcing you into uncomfortable debt. Our team guides you through each step, from choosing your stone and setting to finalizing your custom design and managing your payment schedule. Whether you’re just beginning your search or ready to commit, we’re here to help you build a plan that works as beautifully as the ring itself. Start exploring your options at Bel Viaggio Designs today.

Frequently asked questions

What’s the difference between BNPL and layaway for jewelry?

BNPL lets you take home the ring immediately and pay over time, while layaway requires full payment before you receive the jewelry. Both are lower-risk than traditional financing, according to engagement ring financing basics.

Will applying for a payment plan hurt my credit?

Most BNPL plans use a soft credit check and won’t affect your score, but some longer-term in-house financing involves a hard pull. Choosing soft-check BNPL options protects your credit while still giving you flexibility.

How much down payment is typical for jewelry financing?

Most jewelers require between 20% and 50% of the total jewelry cost as a down payment, which also reduces the amount you’re financing and the interest you’ll pay overall.

What risks should I watch out for in jewelry payment plans?

Watch for high APRs after promo periods, deferred interest traps, and penalties for missed payments. Always read the full terms before signing, and ask specifically whether interest is waived or merely deferred.

Recommended

- Step-by-step ethical engagement ring workflow 2026 – Bel Viaggio Designs, LLC

- Smart Tips for Shopping On-Sale Jewelry Ethically and Affordably – Bel Viaggio Designs, LLC

- Custom ring guide: step-by-step ethical luxury (2026) – Bel Viaggio Designs, LLC

- How to select bespoke jewelry for life’s milestones – Bel Viaggio Designs, LLC